Global Diamond Markets Show Strength in Premium Categories in 2026

Home

News And Media Global Diamond Markets Show Strength in Premium Categories in 2026 SHOP NOWHome

News And Media Global Diamond Markets Show Strength in Premium Categories in 2026 SHOP NOWJun, 19, 2026 by Archit Mohanty 0 Comments

The global diamond industry is undergoing a profound transformation in 2026. After three consecutive years of decline, the market is showing clear signs of recovery but not across the board.

A pronounced polarization has emerged, with premium categories commanding robust demand while commercial-grade stones face persistent headwinds. This analysis examines the current state of global diamond markets, regional dynamics, shape trends, and what these developments mean for buyers, sellers, and investors in the year ahead.

The global diamond market entered 2026 with cautious optimism. The price divergence between commercial and premium diamonds has become one of the defining features of the current market landscape. Commercial diamond prices remain approximately 15% to 30% lower compared to their 2022 peaks, reflecting sustained pressure from laboratory-grown alternatives and shifting consumer preferences.

However, premium diamonds specifically those in the D–F color range with VS clarity and higher are showing much stronger performance. These categories have achieved stable pricing, with some segments experiencing up to 5% price recovery. According to Alrosa, the segment of stones over 3 carats has remained the most stable, with prices for 5-carat diamonds climbing 8.4% quarter-on-quarter in early 2026.

The Diamond Index tells a story of stark contrast. While the 1-carat RAPI fell 9.9% in 2025, the index for 0.30-carat stones slumped 20.3%, and 0.50-carat prices tumbled 26%. Larger stones remained notably resilient, with the 3-carat index edging up even as smaller goods saw sharp corrections.

The global natural diamond market is projected at approximately $112 billion in 2026, with natural diamonds leading premium segments. Research and Markets estimates the global diamond market size was valued at USD 42.74 billion in 2025 and is projected to reach USD 53.16 billion by 2033, growing at a CAGR of 2.7%.

Supply constraints are playing a significant role in the market's recovery. Global natural diamond production is forecast to moderately rebound to around 105 million carats in 2026, but this remains significantly below the peak of over 150 million carats seen just nine years ago.

Major producers have adjusted their production guidance downward. De Beers now targets 21–26 million carats in 2026, down from a previous 26–29 million carats. In the first quarter of 2026, the company reported a 17% rise in rough diamond production to 7.1 million carats, driven by higher volumes from Canada and South Africa. However, the company continues to monitor rough diamond trading conditions to align output with prevailing demand.

The supply-demand imbalance is most acute in premium categories. A detailed analysis of global inventory shows that D–F color diamonds with IF–VVS clarity account for only 14.6% of total available inventory yet represent 20.9% of all buyer searches. Across several premium categories, search demand for high-end natural diamonds exceeds supply by an estimated 30% to 40%.

The US market remains the global driver of diamond demand, with positive sentiment continuing after the Las Vegas shows. Round diamonds above 2 carats in G–J colors and VS–SI clarities are selling well. The market shows particular strength for elongated fancy shapes in the 2 to 4 carat range, G–I, VS–SI categories, which remain in short supply. Interest in radiant cuts is growing.

Fancy Yellow and Fancy Intense Yellow diamonds are experiencing strong demand, particularly in long cushions, radiants, and ovals, driven by big-brand advertising. The US market also shows solid demand for elongated ovals of good shape and quality in D–I, VS–SI categories.

Signet's fiscal 2026 sales increased 2% to $6.8 billion, with profit surging 381% to $294 million. Notably, Signet estimates natural diamonds accounting for 70% of overall engagement-market revenue and over 90% of the $5,000+ price range.

Trading in Belgium remains relatively quiet, though sentiment has improved. Buyers are making more inquiries compared to recent weeks, and many are watching the Hong Kong show closely for market direction. Pear and oval diamonds in the 2 to 3-carat range are standing out as particularly strong performers.

Business activity in Israel remains slow as the local security situation continues to impact the market. The ongoing geopolitical challenges have dampened trading volumes, though the underlying demand structure remains intact.

Indian manufacturers are facing significant pressure from rising rough prices and limited availability. Polished inventories are tightening in select categories, especially 2 carat and larger. Currency movements have added further uncertainty, with the rupee recovering 1.7% in the past month to INR 95 per USD.

The export landscape reflects these challenges. Indian cut and polished diamond exports declined by 8.76% to $8.20 billion during April–November 2025. ICRA expects Indian CPD exports to further decline by 7–10% in fiscal 2026. However, the industry is looking ahead with confidence to the expected bilateral trade agreement between India and the USA.

Despite these headwinds, India has overtaken China and Japan to become the world's second-largest diamond jewellery market, capturing 12% of global demand, according to the 2025 Diamond Acquisition Study by De Beers Group. The domestic natural diamond jewellery market is valued at ₹49,700 crore and is projected to reach ₹150,000 crore by 2030.

Hong Kong dealers are actively preparing for Jewellery & Gem Asia Hong Kong (June 18–21, 2026). Exhibitors expect the fair will attract serious buyers focused on large diamonds and gemstones. Long fancy shapes in 2 carat and larger are the best-performing categories, particularly D–F, IF–VVS, as wealthy mainland clients seek luxury and bespoke jewelry.

Diamonds were the most in-demand stone at recent Hong Kong shows at 29%, followed by rubies at 25% and pearls at 20%, according to a survey by the Hong Kong Trade Development Council. Trendy fashion jewelry (57%) showed the strongest growth potential, followed by precious jewelry (35%) and designer jewelry (21%). Yellow gold (40%) was the most popular precious metal.

Buyers across many markets are becoming more selective. Certified diamonds, larger sizes, and well-cut fancy shapes continue to command premiums, while exceptional quality remains difficult to find.

Round brilliant diamonds continue to dominate the market, maintaining approximately 55% to 60% global share. However, fancy shapes are gaining significant momentum, reshaping consumer preferences in 2026.

According to industry sales data, oval diamonds trail rounds with 11.6% market share, making them the most popular fancy shape. Pear accounts for 5.9%, emerald for 5.7%, radiant for 5.3%, and cushion for 3.7%.

In the premium segment, particularly for stones of 2 carats and larger, long fancy shapes are consistently outperforming rounds. Long cushion cuts are particularly noteworthy, trading at a 20% to 25% premium over their square counterparts.

Long fancy shapes such as ovals, marquises, and emeralds are doing better than rounds in 2 carat and larger sizes. High-quality marquises, long radiants, and long cushions are in short supply. The marquise is now the most expensive fancy shape.

The Natural Diamond Council's 2025 trends report found that round brilliant diamonds led engagement ring sales at 62%, while the marquise shape recorded 12% year-on-year growth, fueled by celebrity interest in elongated, personalized designs.

A significant development on the horizon: the Gemological Institute of America (GIA) plans to introduce cut grades for marquise, oval, and pear-shaped diamonds starting in 2027.

This expansion beyond round brilliants which currently receive cut grades will provide unprecedented standardization for fancy shapes. The lab will start introducing the parameters in 2026 and launch the system formally in 2027.

The fancy color diamond market continues to demonstrate resilience and relative insulation from broader macroeconomic pressures. According to the Fancy Color Research Foundation (FCRF), the overall Fancy Color Diamond Index remained unchanged in Q3 2025, following a 0.5% decline in Q2 and a 0.3% decrease in Q1. This marks the first quarter of price stability after two consecutive declines.

For the full year 2025, fancy-color diamond prices edged down just 1%, a minimal shift that reflects stability. Yellow fancy-color stones recorded the largest full-year decline at 1.9%. However, fancy-intense-yellow diamonds weighing 1 and 1.5 carats each rose 1.1% during Q4 2025.

Blue diamonds fell 0.7% during the year and advanced 0.3% in Q4 2025, the only color to record an increase. Leading the color were 8-carat fancy-vivid-blue diamonds with a 2.1% rise.

Pink diamonds showed mixed performance. While prices slipped 0.7% for the year, strong performances came from 2-carat fancy-intense pinks (up 1.3%) and 1-carat fancy-vivid pinks (up 0.8%). Since the FCRF began collecting data in 2005, pink diamonds have advanced 391%, blue diamonds have grown 242%, and yellows have gained 47%.

The Fancy Color Research Foundation (FCRF) notes that consistent with previous quarters, the market showed continued selective demand, with saturation, rarity, and size influencing prices.

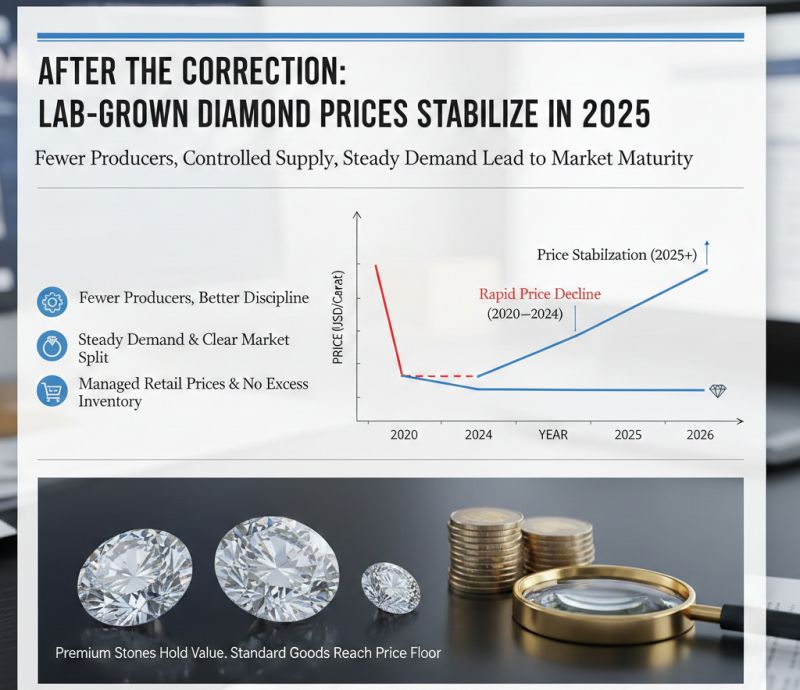

The laboratory-grown diamond market has experienced a dramatic price correction that is reshaping the entire diamond industry. The average wholesale price of one-carat and two-carat lab-grown diamonds has fallen by as much as 96% since 2018.

A 1.5-carat lab-grown diamond that cost $10,750 in 2015 is priced at just $1,455 in 2025 an 86% decline in a decade. The Natural Diamond Council reports that lab-grown diamond prices have dropped over 90%, with unprecedented high retailer margins.

Man-made diamonds have captured about a 25% share of global diamond demand by value spent, up from nil ten years ago. However, the collapse in lab-grown diamond prices has started to undermine consumer confidence in synthetic gems.

Experts warn that the price of lab-grown diamonds could drop so low that they become fashion accessories that no longer compete with natural diamonds, especially in the key bridal market. Natural diamonds currently average $760 per carat, while lab-grown diamonds average just $60.

Investment-grade diamonds are emerging as an increasingly attractive asset class. Alrosa reported that sales of investment diamonds increased 40% in 2025 compared with the previous year. Annual returns for the strongest-performing categories ranged between 12.2% and 14.7% in dollar terms.

Prices for investment-grade goods (2 carats to 10 carats) increased by between 6% and 9% during the first three trading sessions of 2026. Industry forecasts suggest a moderate price recovery of 5–12% for cut diamonds through 2026, particularly for stones above 1 carat with D–H color and VS2 or better clarity.

The 5-carat diamond category has been highlighted as a top investment performer. The growing polarization between commercial-grade and investment-grade stones continues to define the market.

Younger consumers are redefining the codes of diamond luxury. Gen Z and Millennials now represent the majority of global diamond jewellery demand. A significant portion anticipate purchasing or receiving natural diamond jewellery within the next 24 months.

Speciality jeweller sales of natural diamonds grew by 2.1% in 2025, while the average price of natural diamond jewellery increased by 10%. This suggests that consumers are trading up to higher-quality pieces rather than purchasing more units.

The aesthetic that appeals to younger consumers, particularly Gen Z, is driving demand for fancy shapes and unique designs. The Natural Diamond Council notes that younger customers are not necessarily interested in absolutely flawless gems; rather, many are looking for gems that charm in their distinctive and rare "perfect imperfection".

Elongated diamond cuts oval, marquise, and pear are among the strongest trending shapes in 2026, valued for their ability to create the visual illusion of a larger stone and flatter the finger with a lengthening effect.

Buyers are becoming increasingly discerning about certification. Diamonds without certification are becoming hard to sell in the mainland Chinese market. Certified diamonds, larger sizes, and well-cut fancy shapes continue to command premiums.

The diamond market has downsized in response to lower sales and will continue to do so. The sector must maintain supply discipline to ensure a recovery happens, since efforts to promote demand will likely take years to pay off.

The US-India trade deal announced in February boosted sentiment in the Indian diamond sector. This agreement is expected to provide significant relief for gem and jewellery exports.

The industry remains watchful on several fronts: the proposed sale of De Beers, sanctions on Russia, high gold prices, and the prospects of a US-India trade agreement. Current demand patterns are expected to persist through 2026.

De Beers continues to monitor rough diamond trading conditions to align output with prevailing demand. The company's production guidance for 2026 remains at 21–26 million carats.

The global diamond market in 2026 is characterized by a clear and growing polarization. Premium categories larger stones, higher clarities, better colors, and well-cut fancy shapes are demonstrating remarkable strength. Commercial-grade diamonds face continued pressure from lab-grown alternatives and shifting consumer preferences.

For buyers, this means that exceptional quality comes at a premium, but also offers better value retention. For sellers, the message is clear: differentiation through quality, certification, and cut precision is essential for success in this evolving market.

The recovery is real, but it is not uniform. Those who understand and adapt to the new market dynamics, where premium commands premium and ordinary faces headwinds will be best positioned to thrive in the years ahead.

Natural Diamond Market 2026 – An in-depth analysis of the recovery and stabilization of the global natural diamond market in 2026

Shop Natural Diamonds – Explore our collection of certified natural diamonds from trusted sources worldwide

Shop Gemstones – Discover high-quality gemstones at unbeatable prices through our global marketplace

Sell on CaratX – Start selling diamonds and jewelry to buyers across 18+ international countries

The 2026 Fancy Shape Diamond Market Revolution: Global Shifts Are Redefining the 2‑Carat+ Landscape – A comprehensive analysis of how elongated fancy shapes like Ovals, Marquises, and Emeralds are outperforming rounds in the 2-carat and above segment.

The Diamond Market Shift: Why Long Fancy Shapes Are Outperforming Rounds in 2026 – An in-depth market update on why "Long" is the new "Round," examining how shapes like Ovals, Marquises, and Radiants are becoming primary investments for savvy buyers in the 2-carat+ category.

Fancy Shape Diamonds: A Deep Dive into Market Trends, Consumer Preferences, and Strategic Insights – A detailed examination of what's driving demand for specific fancy shapes, why certain stones command substantial premiums, and how to navigate this evolving landscape.

Why Fancy Color Diamonds Are Capturing Attention in 2026: The Complete Investor & Collector’s Guide – An authoritative guide to the GIA fancy color grading scale, explaining why Fancy Vivid, Fancy Intense, and Fancy Light diamonds represent distinct investment opportunities.

The Diamond Inventory Paradox: Why Vaults Overflow While Demand Goes Unmet – An analysis of the industry's structural contradiction: drowning in diamonds nobody wants while desperately short on the diamonds everyone seeks.

The Rise of Elongated Diamonds: Market Trends, Pricing & Sourcing Guide – A comprehensive guide to understanding the psychological and market factors driving the surge in demand for elongated fancy shapes.

Diamond Carat Size Guide: Charts, Real-Life Examples & Buying Tips – Learn what carat size really means, how common carat weights look on the hand, and how to avoid overpaying for "dead" weight.

CVD vs. HPHT: How Lab-Grown Diamonds Are Made – A detailed comparison of the two primary methods used to create lab-grown diamonds, explaining the pros and cons of each.

Understanding Diamond Color – A Comprehensive Guide – Everything you need to know about the diamond color grading scale and how it influences price.

Raw Diamond Guide: How to Identify, Value, and Buy Rough Stones with Confidence – A practical guide to identifying, assessing, and buying raw diamonds for collecting, investing, or custom jewelry design.

Premium diamonds (D–F color, IF–VVS clarity, 2 carats and larger) are outperforming due to supply constraints, limited production from major miners, and shifting consumer preferences toward higher-quality, investment-grade stones. Commercial-grade diamonds face pressure from lab-grown alternatives.

Long fancy shapes particularly ovals, marquises, emeralds, radiants, and elongated cushions are in highest demand, especially in 2 carat and larger sizes. Long cushions are trading at a 20% to 25% premium over square cushions.

Lab-grown diamonds have captured approximately 25% of global diamond demand by value. However, their prices have collapsed by up to 96% since 2018, undermining consumer confidence and potentially driving buyers back to natural diamonds.

Industry forecasts suggest a moderate price recovery of 5–12% for cut diamonds through 2026, particularly for stones above 1 carat with D–H color and VS2 or better clarity. Premium categories are expected to continue outperforming commercial grades.

The United States remains the strongest market, followed by India (now the world's second-largest diamond jewellery market). Hong Kong and mainland China show selective demand for large, high-quality stones.

Investment-grade diamonds typically fall in the 2-carat to 10-carat range with D–H color and VS2 or better clarity. Certification from reputable laboratories like GIA is essential. Fancy shapes with excellent proportions and symmetry command premiums.

Follow CaratX for more insightful and educational content on the global diamond and jewelry markets.

Jun, 18, 2026

Aug, 06, 2022

Aug, 06, 2022

0 Comments

Please login to leave a reply.