India's Diamond Retail Market Revolution: The $8 Billion Industry Poised for Explosive Growth

Home

Education Blog India's Diamond Retail Market Revolution: The $8 Billion Industry Poised for Explosive Growth SHOP NOWHome

Education Blog India's Diamond Retail Market Revolution: The $8 Billion Industry Poised for Explosive Growth SHOP NOWJan, 29, 2026 by Archit Mohanty 0 Comments

The Indian diamond jewelry market stands at a fascinating crossroads. Valued at over $8 billion and expanding at a robust 8-10% annually, this industry is experiencing a transformation that goes far beyond simple revenue growth. What we're witnessing is a fundamental restructuring of how diamonds are sold, who's buying them, and where these transactions are taking place across the subcontinent.

India's relationship with diamonds runs deeper than most realize. As the world's largest diamond cutting and polishing center, India processes an astounding 90% of all diamonds globally. According to the Gemological Institute of America, the city of Surat alone employs over 700,000 skilled artisans who transform rough stones into brilliant gems that sparkle in jewelry stores from Mumbai to Manhattan.

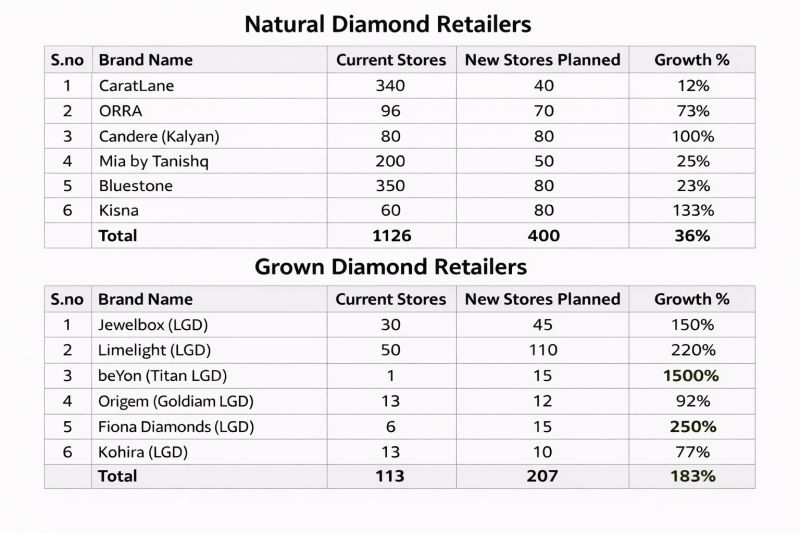

This manufacturing dominance has created a unique ecosystem. Indian craftsmen possess centuries of inherited knowledge in diamond processing, yet the domestic retail infrastructure has historically lagged behind. The organized diamond retail market currently represents only 30-35% of total sales, a striking gap that presents enormous growth potential for forward-thinking retailers.

The fragmented nature of India's diamond retail landscape is rapidly consolidating. Traditional family-owned jewelers, who have dominated the market for generations, now face competition from organized retail chains equipped with sophisticated inventory management systems, standardized pricing, and aggressive expansion strategies.

Perhaps no trend has shaken the industry more profoundly than the emergence of lab-grown diamonds (LGDs). These diamonds, created through advanced technological processes that replicate natural diamond formation, have moved from niche curiosity to mainstream alternative in less than three years.

The economics are compelling. Lab-grown diamonds typically cost 40-60% less than their natural counterparts of comparable quality. For a young professional couple planning their wedding, this price differential can mean the difference between a half-carat and a full-carat diamond a psychologically significant threshold in a market where size still matters.

Even trained gemologists require specialized equipment to distinguish between them. This scientific validation has given consumers confidence that they're not compromising on quality when choosing lab-grown options.

Major retailers have responded by launching dedicated LGD brands or product lines. CaratX's natural diamond collection now sits alongside lab-grown alternatives, offering consumers choice and transparency. The platform's commitment to certification and detailed product information helps buyers make informed decisions regardless of their diamond preference.

According to industry reports from the Gemological Institute of America's educational resources, the lab-grown diamond segment in India is projected to grow at over 20% annually through 2027, significantly outpacing natural diamond growth rates.

The most significant retail shift is geographic. Tier 2 and Tier 3 cities now contribute 45-50% of jewelry sales, fundamentally altering expansion strategies. Cities like Coimbatore, Jaipur, Nagpur, Indore, and Lucknow have emerged as critical battlegrounds for market share.

Rather than concentrating in megacities, economic growth is dispersing across hundreds of medium-sized urban centers, each with rising middle-class populations hungry for branded retail experiences.

These emerging markets present distinct advantages. Real estate costs remain significantly lower than metro areas, reducing the barrier to profitable store operations. Competition is less intense, allowing new entrants to establish brand presence before markets become saturated. Consumers in these cities increasingly prefer organized retail with assured quality over traditional jewelers, creating openings for branded chains.

CaratX's seller registration platform has empowered local jewelers in these markets to access international buyers, bridging the gap between traditional craftsmanship and global e-commerce infrastructure. This democratization of access represents a parallel revolution happening alongside physical retail expansion.

Wedding jewelry purchases drive 65-70% of diamond sales in India, according to industry estimates. Understanding this cultural reality is essential. Unlike Western markets where diamond purchases are distributed across occasions anniversaries, birthdays, self-purchase Indian diamond buying concentrates intensely around weddings.

Traditional diamond brands are opening 100+ stores to defend market position. Lab-grown diamond specialists are building store networks from scratch. Independent jewelers are modernizing storefronts to compete. The result is an unprecedented wave of physical retail expansion in an era when e-commerce supposedly dominates.

Why physical stores? Despite digital growth, physical stores still drive 85% of diamond jewelry sales in India. The reasons are cultural and practical. Diamond purchases represent significant investments, often requiring family consultation. Customers want to see, touch, and compare stones under proper lighting. Trust remains paramount, and physical presence signals permanence and accountability.

However, not all store formats succeed equally. The critical variables determining success include:

Location Strategy: Mall locations offer foot traffic and aspirational brand association but command premium rents. High street locations in commercial districts provide visibility at lower costs but may lack the shopping environment that encourages browsing. Neighborhood stores in affluent residential areas capture repeat customers but limit walk-in discovery.

Store Profitability Per Square Foot: The Indian retail mantra holds that revenue per square foot determines viability. Diamond retailers typically require ₹40,000-60,000 ($480-720) per square foot annually to sustain operations in prime locations. Achieving this demands careful inventory curation, staff training, and conversion rate optimization.

Inventory Turnover: Unlike apparel retail where trends change seasonally, diamond jewelry can sit in inventory for extended periods. CaratX's gemstone marketplace demonstrates how digital platforms can accelerate inventory movement by connecting sellers with a broader buyer base, reducing the capital locked in slow-moving stock.

Brand Positioning: In a market spanning from budget-conscious first-time buyers to ultra-high-net-worth collectors, clear positioning prevents dilution. Brands must decide whether they're competing on price, exclusivity, design innovation, or ethical sourcing and communicate consistently across all touchpoints.

The statistic that organized retail represents only 30-35% of India's diamond market deserves deeper examination. In mature markets like the United States, organized retail exceeds 70% of jewelry sales. India's lower penetration reflects historical factors family jewelers with multi-generational customer relationships, trust networks based on community ties, and informal pricing that accommodated negotiation.

However, demographic shifts are rewriting these patterns. Younger consumers, particularly millennials and Gen Z, demonstrate strong preferences for transparent pricing, quality certifications, and brand reputation over personal relationships with jewelers. Educational initiatives from organizations like the Gemological Institute of America have increased consumer knowledge about diamond grading, making standardized certifications more valuable.

This creates a window for organized retailers to capture disproportionate share of market growth. Even if the total market grows at 8-10% annually, organized retail within that market could grow at 15-20% as it captures both new customers and those switching from unorganized channels.

Platforms like CaratX's international marketplace exemplify this organized approach, offering sellers access to buyers across 18+ countries with standardized processes, secure payments, and quality assurance mechanisms that would be impossible to replicate in traditional unorganized trade.

India's dominance in diamond cutting creates structural advantages for domestic retailers. Shorter supply chains reduce costs. Direct relationships with manufacturers enable customization and faster inventory replenishment. Understanding of manufacturing processes allows better quality control.

Research published by Harvard Business School on supply chain optimization highlights how vertical integration or close manufacturer relationships provide competitive advantages in commodity markets. Indian diamond retailers can leverage proximity to manufacturing hubs in ways international competitors cannot easily replicate.

This advantage extends to lab-grown diamonds as well. India is rapidly developing LGD manufacturing capacity, with facilities in Gujarat and Tamil Nadu producing commercial quantities. India is positioned to become a major global producer of lab-grown diamonds, potentially replicating its natural diamond processing dominance in this emerging category.

CaratX's seller plans for jewelry connect manufacturers directly with international retail channels, eliminating intermediaries and enabling Indian manufacturers to capture more value from their expertise. This direct-to-consumer and direct-to-retailer model represents the future of the industry.

Online-to-Offline Integration: Customers can browse inventory online, schedule appointments, and even reserve specific pieces for in-store viewing, making store visits more efficient and conversion-focused.

CaratX's pricing structure reflects this omnichannel reality, offering sellers tools to manage both B2B and B2C channels through a unified platform. The ability to reach buyers across multiple channels without maintaining separate systems reduces operational complexity for smaller retailers.

The window for establishing market position is narrowing. As organized retail consolidates and prime locations in emerging cities get claimed, latecomers will face higher entry costs and entrenched competition. The next 24 months will determine market structure for the next decade.

For Traditional Jewelers: The question is whether to expand aggressively, accept regional specialization, or exit to larger players. Many family businesses face succession challenges as younger generations pursue alternative careers, creating opportunities for consolidation.

For Lab-Grown Diamond Brands: Moving from novelty to mainstream requires establishing trust, building brand equity, and educating consumers about value propositions beyond price. Sustainability and ethical sourcing narratives need development to resonate with Indian sensibilities.

For Investors: The sector offers high-growth opportunities but requires understanding of local market dynamics, real estate strategy, and jewelry industry economics that differ substantially from other retail categories.

For Consumers: Increasing options and transparency empower better purchasing decisions, but also require more sophisticated evaluation of quality, pricing, and value.

Platforms like CaratX are positioned to benefit regardless of which specific brands or formats succeed, as they provide infrastructure that serves the entire ecosystem connecting manufacturers, retailers, and consumers across traditional and emerging diamond categories.

Diamond retail requires substantial working capital due to inventory investment. A typical store might carry ₹2-5 crore ($240,000-600,000) in inventory, with expectations to turn that inventory 1.5-2 times annually. This creates significant capital requirements for multi-store expansion.

Different financing models are emerging:

Consignment Arrangements: Manufacturers place inventory in retail stores, retaining ownership until sale. This reduces retailer capital requirements but limits margin potential.

Inventory Financing: Specialized lenders provide working capital secured by diamond inventory, enabling retailers to carry broader selections without tying up operational capital.

Franchise Models: Brand owners enable expansion through franchisees who invest capital while the brand maintains control over merchandising, training, and standards.

Marketplace Models: Platforms like CaratX enable sellers to list inventory accessible to global buyers without physical store investments, representing a capital-light alternative to traditional retail expansion.

Understanding these financial dynamics is essential for assessing which retailers can sustain aggressive expansion plans and which may overextend. Industry observers predict consolidation as undercapitalized players exit or merge.

India's diversity means that successful strategies vary dramatically by region. Southern markets traditionally prefer gold-heavy jewelry with diamonds as accents. Western markets embrace contemporary designs with diamond prominence. Northern markets blend traditional and modern aesthetics. Eastern markets have distinct festival-driven purchase patterns.

Store design, inventory composition, marketing messaging, and pricing strategies must accommodate these regional preferences. National chains attempting uniform approaches risk local irrelevance. Conversely, purely local players may lack economies of scale for competitive pricing and brand investment.

The most successful retailers are developing frameworks that allow regional customization within overall brand consistency similar to how international brands adapt to India while maintaining core identity.

Current market leaders include established jewelry chains expanding diamond offerings, pure-play diamond specialists building national presence, and international luxury brands serving ultra-premium segments. Each approaches the opportunity differently.

Established Jewelry Retailers: Leverage existing customer relationships, store networks, and brand equity. They're adding diamond categories to capture share of growing demand. Their challenge is avoiding perception as old-fashioned relative to newer entrants.

Pure-Play Diamond Specialists: Build focused expertise and clear positioning in consumer minds. Unencumbered by legacy operations, they can optimize everything for diamond retail specifically. Their challenge is building brand awareness and trust without the heritage advantage of established players.

International Luxury Brands: Command premium pricing and attract aspirational consumers. Their challenge is adapting to price sensitivity and regional preferences in a market culturally and economically distinct from Western markets where they built their brands.

Lab-Grown Diamond Specialists: Capture price-conscious and values-driven consumers. Their rapid growth has exceeded initial projections, but sustainability depends on maintaining price advantages as LGD production scales and potentially becomes commoditized.

Online-First Brands: Platforms like CaratX compete through selection, convenience, and competitive pricing enabled by lower overhead. They're building hybrid models with physical touchpoints for high-value purchases while maintaining digital advantages for discovery and research.

For investors and industry participants, India's diamond retail market presents compelling characteristics:

Large and Growing Market Size: At $8+ billion and growing 8-10% annually, the market offers significant revenue potential.

Low Organized Penetration: With organized retail at 30-35%, substantial market share remains available for capture.

Favorable Demographics: A large and growing middle class with rising incomes and aspirational consumption patterns.

Cultural Affinity: Deep cultural connection to jewelry and diamonds, particularly for weddings and celebrations.

Manufacturing Infrastructure: Proximity to the world's largest diamond processing center creates structural advantages.

Digital Adoption: Rapidly increasing smartphone and internet penetration enabling omnichannel strategies.

India's diamond retail market stands at an inflection point. The confluence of rising incomes, demographic advantages, manufacturing infrastructure, evolving consumer preferences, and technological enablement creates conditions for explosive growth. However, growth alone doesn't guarantee success for individual participants.

The retailers who will thrive are those who:

Choose locations strategically based on target customer concentration rather than simply chasing the most stores

Develop operational excellence in inventory management, staff training, and customer experience

Build brands with clear positioning that resonates with specific customer segments

Integrate digital and physical channels to serve customers across their purchase journey

Maintain financial discipline even amid pressure for rapid expansion

Stay adaptive as market conditions, consumer preferences, and competitive dynamics evolve

For an industry built on beauty, rarity, and emotion, the next chapter will be defined by operational excellence, strategic clarity, and deep customer understanding. The diamonds may be timeless, but the retail models serving them must be thoroughly modern.

Whether you're a manufacturer looking to reach global markets through platforms like CaratX, a retailer planning expansion, an investor evaluating opportunities, or a consumer preparing for a significant purchase, understanding these dynamics positions you to navigate the transformation ahead.

The $8 billion market of today is building toward something substantially larger. How that growth gets captured, who captures it, and what the resulting industry structure looks like remains to be determined. What's certain is that the next 24 months will set the trajectory for the next decade.

Q: What's the difference between natural and lab-grown diamonds?

A: Chemically, physically, and optically, lab-grown diamonds are identical to natural diamonds. Both are pure carbon crystallized in the same atomic structure. The difference is origin: natural diamonds formed over billions of years deep in the earth, while lab-grown diamonds are created in weeks using high-pressure high-temperature (HPHT) or chemical vapor deposition (CVD) processes. Lab-grown diamonds typically cost 40-60% less but are scientifically indistinguishable from natural diamonds without specialized equipment.

Q: Why are physical stores still dominant when e-commerce is growing?

A: Diamond purchases represent significant emotional and financial investments. Customers want to see stones in person, compare options under proper lighting, and have confidence in seller credibility before committing thousands of dollars. Additionally, Indian culture emphasizes family consultation for jewelry purchases, which occurs more naturally in physical environments. While digital research increasingly influences decisions, the final transaction usually happens in stores hence the 85% physical sales figure.

Q: Are diamonds from India lower quality than diamonds from other countries?

A: No. India doesn't mine significant diamonds it processes them. India cuts and polishes 90% of the world's diamonds regardless of where they were mined. The quality of a finished diamond depends on the original rough stone and the skill of the craftsmen. Indian diamond processing is globally recognized for expertise and precision. CaratX's natural diamond selection includes certified stones meeting international quality standards.

Q: How can I verify diamond quality when shopping?

A: Request certification from recognized gemological laboratories GIA (Gemological Institute of America), IGI (International Gemological Institute), or HRD (Hoge Raad voor Diamant) are the most trusted. Certificates detail the "4 Cs": cut, color, clarity, and carat weight. For lab-grown diamonds, certification should explicitly identify them as such. Reputable retailers provide certificates automatically; if a seller hesitates to provide certification, consider that a warning sign.

Q: What's driving the expansion into Tier 2 and Tier 3 cities?

A: Three primary factors: (1) Rising incomes in these cities creating affluent middle-class populations; (2) Lower real estate costs enabling profitable stores with lower sales volumes; (3) Less competitive intensity allowing new entrants to establish presence. These cities now contribute 45-50% of jewelry sales, making them essential for retailers pursuing national scale.

Q: Should I buy natural or lab-grown diamonds?

A: This depends on your priorities. If you value natural rarity and traditional prestige, or view diamonds as financial assets, natural diamonds are preferable. If you prioritize maximizing size and quality within a budget, or have environmental concerns about mining, lab-grown diamonds offer advantages. Both are real diamonds. The CaratX marketplace offers both options with transparent information to help you decide based on your specific values and circumstances.

Aug, 06, 2022

Aug, 06, 2022

Oct, 09, 2024

0 Comments

Please login to leave a reply.