Executive Summary:

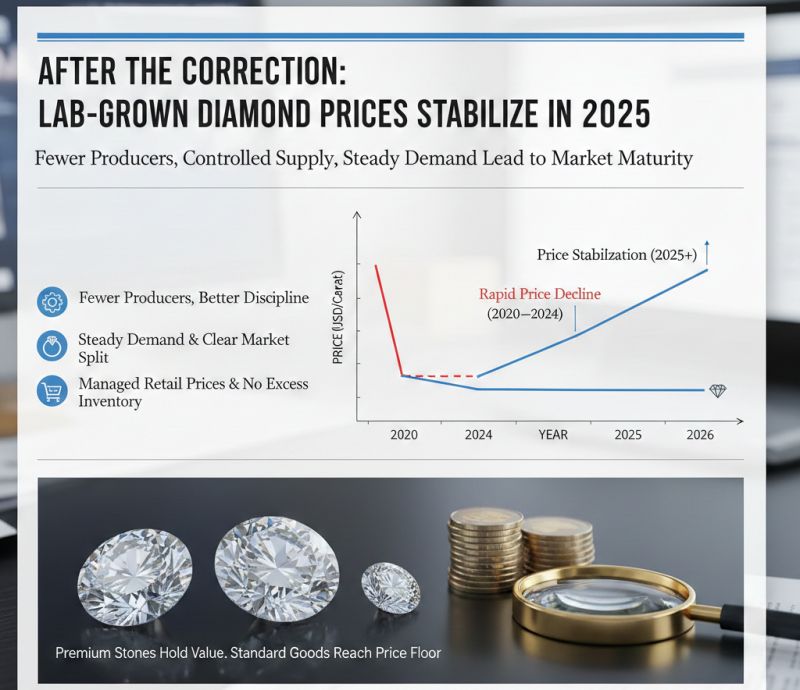

The lab-grown diamond industry has undergone one of the most dramatic transformations in modern luxury goods history. From peak prices exceeding $4,000 per carat in 2018, the market experienced a near-total collapse, with prices plummeting approximately 96% to stabilize around $168 per carat by early 2025. This precipitous decline, often termed "The Great Correction," fundamentally reshaped the industry's structure, consumer perception, and economic model. However, 2025 marks a decisive turning point not toward renewed explosive growth, but toward sustainable stabilization.

This in-depth analysis examines the complex interplay of technological, economic, and behavioral factors that have halted the price freefall and established a foundation for the industry's mature phase, characterized by rational competition, clear market segmentation, and predictable demand patterns.

The Anatomy of the Price Collapse (2018-2024)

Technological Democratization and Production Overcapacity -

The initial price collapse stemmed from the fundamental economics of synthetic production. Unlike natural diamonds constrained by geological scarcity and extraction costs, lab-grown diamond production benefits from continuous technological improvement and scalability. The widespread adoption of both Chemical Vapor Deposition (CVD) and High Pressure High Temperature (HPHT) methods led to a production surge.

According to industry analyses, global production capacity increased by over 300% between 2020 and 2023, far outpacing demand growth. This created a classic supply-demand imbalance, where manufacturers were compelled to cut prices to move inventory, triggering a downward spiral.

The learning curve effect in manufacturing technology played a crucial role. As documented , production efficiencies for crystalline materials typically improve by 20-30% with each doubling of cumulative output. Lab-grown diamonds followed this pattern precisely, with production costs falling dramatically even as quality improved. This created a dual pressure on prices: more stones entering the market and lower break-even points for producers.

The Inventory Glut and Distribution Channel Pressures -

By 2023, the industry faced an unprecedented inventory overhang. Estimates suggest that at the peak of the imbalance, the global inventory of polished lab-grown diamonds represented 18-24 months of demand. This excess stock permeated every level of the supply chain, from manufacturers to wholesalers to retailers. Faced with carrying costs and the risk of technological obsolescence (as newer production runs yielded better quality at lower costs), channel participants engaged in distress selling.

This inventory liquidation created a psychological shift in the market. As noted by Edahn Golan, a leading diamond industry analyst, "When prices decline consistently for 24 consecutive months, buyers cease to see current prices as a bargain and instead anticipate further declines." This deflationary mindset became entrenched among both trade buyers and consumers, exacerbating the downward price pressure as everyone sought to minimize their exposure to future depreciation.

Erosion of Perceived Value and Luxury Status -

The rapid price decline fundamentally altered consumer perception. Initially marketed as "ethical luxury" with premium positioning, lab-grown diamonds increasingly became viewed as industrial commodities rather than luxury goods. The psychological principle of scarcity value, a cornerstone of luxury marketing was completely absent from the lab-grown proposition. As prices fell, the narrative shifted from "affordable luxury" to "disposable fashion," particularly for smaller carat weights.

This perception shift was quantified in consumer research, a luxury goods research firm. Their 2024 study found that while 78% of consumers acknowledged the visual equivalence of lab-grown and natural diamonds, only 23% attributed any "emotional value" to lab-grown stones, compared to 89% for natural diamonds. This emotional/value disconnect created a self-reinforcing cycle: lower prices reduced perceived value, which justified further price reductions in consumers' minds.

The Pillars of 2025 Stabilization -

Industry Consolidation and Manufacturing Discipline -

The shakeout phase of 2023-2024 achieved what market forces typically accomplish: the elimination of marginal producers. Industry estimates suggest that approximately 40% of dedicated lab-grown diamond manufacturers either exited the business or significantly reduced capacity during this period. The survivors share distinct characteristics:

Vertical Integration: Leading producers have invested backward into equipment manufacturing and forward into branding, reducing reliance on commodity trading.

Quality Specialization: Rather than competing across all quality categories, surviving manufacturers have developed specialized competencies. Some focus on premium D-F color, IF-VVS clarity stones for the luxury segment, while others optimize for consistent commercial-grade production.

Production Flexibility: Modern facilities can rapidly scale production up or down by 30-40% in response to market signals, avoiding the inventory builds that characterized earlier years.

This new manufacturing discipline is evident in production data. After quarterly declines throughout 2023, production volumes stabilized in Q4 2024 and have shown only modest single-digit growth in 2025, closely aligned with demand projections rather than capacity-driven oversupply.

Market Bifurcation:

The most significant structural development has been the clear stratification of the market into distinct segments with different economic characteristics:

Premium Segment (Approximately 15% of Market Volume, 30% of Value)

Quality Parameters: Typically stones of 2 carats and above with D-F color, VVS+ clarity, and excellent cut proportions. Often accompanied by supplemental certification from organizations like the Gemological Institute of America (GIA) that includes detailed growth method analysis.

Price Stability: Premium stones have demonstrated price resilience, declining only 10-15% in 2024 compared to 40-50% for commercial goods. In some specialized categories (particularly fancy colors like vivid blues and pinks), prices have remained flat or even appreciated slightly.

Distribution Channels: Primarily sold through specialty jewelers and direct-to-consumer brands that emphasize craftsmanship, design, and brand storytelling rather than competing solely on price.

Commercial Segment (Approximately 85% of Market Volume, 70% of Value)

Quality Parameters: Typically 0.5-2.0 carat stones with G-J color, VS-SI clarity, and good to very good cut. Often sold with basic certification focused on the 4Cs without detailed origin analysis.

Price Floor Establishment: Commercial goods appear to have found a price floor at $100-150 per carat for 1ct equivalents. At this level, they compete directly with high-end cubic zirconia and moissanite while offering the technical advantages of diamond (hardness, refractive index).

Commodity Dynamics: This segment behaves like a true commodity, with prices closely tracking manufacturing input costs (primarily electricity and equipment depreciation) plus a modest margin.

Lab-Grown Diamond Market Segmentation (2025)

1. Premium Segment

Positioning: Design-led, brand-driven, value-focused

Price per carat (1ct equivalent): $500 – $1,200

Price trend (2024–2025): −5% to +2% (largely stable)

Primary distribution channels: Specialty jewelers, DTC brands

Core consumer motivations: Design, brand, sustainability

Expected growth rate (2025): 8–12% annually

Typical gross margins: 50–65%

2. Commercial Segment

Positioning: Volume-led, price-sensitive, fast-turnover

Price per carat (1ct equivalent): $100 – $300

Price trend (2024–2025): −15% to −5% (continued pressure)

Primary distribution channels: Mass merchants, online marketplaces

Core consumer motivations: Price, size, immediate gratification

Expected growth rate (2025): 3–5% annually

Typical gross margins: 20–35%

Retail Strategy Evolution:

Progressive retailers have fundamentally reimagined their approach to lab-grown diamonds, implementing strategies that support price stability:

Merchandising Separation -

Leading jewelry chains now present lab-grown and natural diamonds in physically separate cases with distinct branding, avoiding direct comparison. This "separate but equal" presentation allows each category to communicate its unique value proposition without triggering price-based decision frameworks.

Value-Based Pricing Architecture

Instead of cost-plus pricing, sophisticated retailers employ tiered value architecture:

Good: Basic solitaire settings with commercial-grade stones

Better: Enhanced design elements with better quality stones

Best: Custom designs with premium stones, often accompanied by upgrade programs and lifetime services

This structure allows consumers to trade up within the lab-grown category based on design and craftsmanship rather than simply carat weight.

Experience Bundling -

Forward-thinking retailers bundle lab-grown diamond jewelry with value-added services: complementary redesign after 5 years, lifetime cleaning and inspection, and trade-in programs toward future purchases. These services, while having modest actual cost, significantly enhance perceived value and reduce price sensitivity.

Inventory Normalization and Supply Chain Rationalization -

The inventory correction of 2024 successfully addressed the systemic overhang. Three factors contributed to this normalization:

Production Alignment: Manufacturers reduced output by approximately 35% in Q3-Q4 2024, allowing demand to catch up with supply.

Channel Liquidation: Distributors offered time-limited promotional terms to retailers, accelerating the movement of older inventory.

Demand Absorption: The price points reached in late 2024 stimulated new demand segments, particularly for fashion jewelry and "right hand" rings.

Current inventory levels across the supply chain represent 4-6 weeks of forward demand, a healthy figure that allows for product variety without creating distressed selling pressure. This normalized inventory position represents perhaps the single most important contributor to 2025 price stability.

Demand Maturation and Consumer Behavior -

The Established Consumer Base

Lab-grown diamonds have transitioned from early adoption to mainstream acceptance. The consumer profile has expanded and matured:

Core Segments:

Bridal Market (40% of demand): Still the largest segment, but with altered dynamics. Engagement ring buyers increasingly choose lab-grown for size maximization within budget constraints. The average carat weight for lab-grown engagement stones is 2.1ct versus 1.5ct for natural.

Self-Purchase Fashion (35% of demand): Primarily driven by women aged 25-45 purchasing celebratory or aspirational jewelry for themselves. This segment shows the strongest growth at 15-20% annually.

Male Consumers (15% of demand): A growing segment purchasing lab-grown diamond stud earrings, bracelets, and signet rings.

"Upgraders" (10% of demand): Typically couples marking milestone anniversaries who previously purchased smaller natural diamonds and now want larger stones.

Geographic Demand Patterns -

Demand has stabilized across major markets with distinct characteristics:

United States: The most mature market, representing approximately 50% of global demand. Growth has stabilized at 5-7% annually, with particular strength in fashion jewelry and men's categories.

China: Showing the fastest growth at 20-25% annually, though from a smaller base. Chinese consumers particularly value technological achievement in lab-grown production and show strong preference for larger stones (3+ carats).

India: A complex market where lab-grown diamonds compete with both natural diamonds and traditional gold jewelry. Growth is concentrated in metro areas among younger, Western-influenced consumers.

Europe: The most sustainability-focused market, where environmental claims require rigorous substantiation. Growth is steady at 8-10% annually, led by the UK, Germany, and France.

The Future Trajectory:

Technological Frontiers -

Innovation continues but with a shift from cost reduction to quality enhancement and specialization:

Color Consistency: Advanced control systems now produce more consistent fancy colors, particularly in blues and pinks, opening new design possibilities.

Size Scaling: Commercial production of 10+ carat gem-quality stones has become feasible, creating entirely new product categories.

Material Properties: Research into nitrogen-vacancy center diamonds for quantum computing and other high-tech applications represents a potentially larger market than jewelry, though with different economic characteristics.

Market Coexistence with Natural Diamonds -

The industry has largely moved beyond the adversarial "versus" narrative to recognize complementary coexistence:

Natural Diamonds: Emphasizing geological rarity, heritage, and emotional significance. The natural diamond industry has responded to lab-grown competition by increasing marketing investment (the $20 million/month "Real is Rare" campaign) and emphasizing provenance through blockchain initiatives like the De Beers Tracr platform.

Lab-Grown Diamonds: Positioned as accessible luxury, design freedom, and sustainable choice. The most successful brands avoid comparative messaging and instead focus on their unique advantages: size availability, color options, and contemporary design possibilities.

This coexistence is reflected in retail performance data: stores that carry both categories typically see 30-40% higher overall diamond jewelry sales than those carrying only one category, suggesting they serve complementary rather than competing needs.

Price Outlook and Economic Model -

Looking forward, the economic model for lab-grown diamonds will resemble consumer electronics more than traditional luxury goods:

Continued Moderate Price Declines: Expect 5-10% annual price declines for commercial goods as production efficiencies continue, compared to 40-50% in previous years.

Premium Resilience: Higher quality and specially certified stones will maintain stronger pricing, with declines limited to 0-5% annually.

Value Migration: Economic value will shift from the stone itself to design, branding, and retail experience, with the diamond component representing a decreasing percentage of total jewelry value (currently 30-50% versus 70-80% for natural diamond jewelry).

Conclusion:

The lab-grown diamond industry has emerged from its turbulent adolescence into a more stable maturity. The price freefall has ceased not because of artificial constraints or market manipulation, but through organic economic processes: industry consolidation, demand maturation, inventory normalization, and strategic evolution at retail.

For consumers, this stabilization brings transparency and predictability. The extreme volatility that made purchase timing anxiety-inducing has given way to more stable pricing, allowing buyers to focus on design and emotional resonance rather than arbitrage.

The fundamental transformation is complete: lab-grown diamonds have evolved from disruptive novelty to established category. They haven't replaced natural diamonds but have instead expanded the universe of diamond jewelry, making it accessible to new consumer segments while pushing the entire industry toward greater transparency, innovation, and consumer focus. As the market continues to evolve, this stability provides the foundation for the next phase of innovation and growth.

Explore the new era of diamond jewelry with confidence.

Discover our curated collections of Premium Lab-Grown Diamonds for exceptional quality and value.

Explore the timeless beauty of our Natural Diamond Selection.

For jewelers and retailers looking to capitalize on this stabilized market, learn about our B2B Marketplace Solutions to access a global network of buyers.